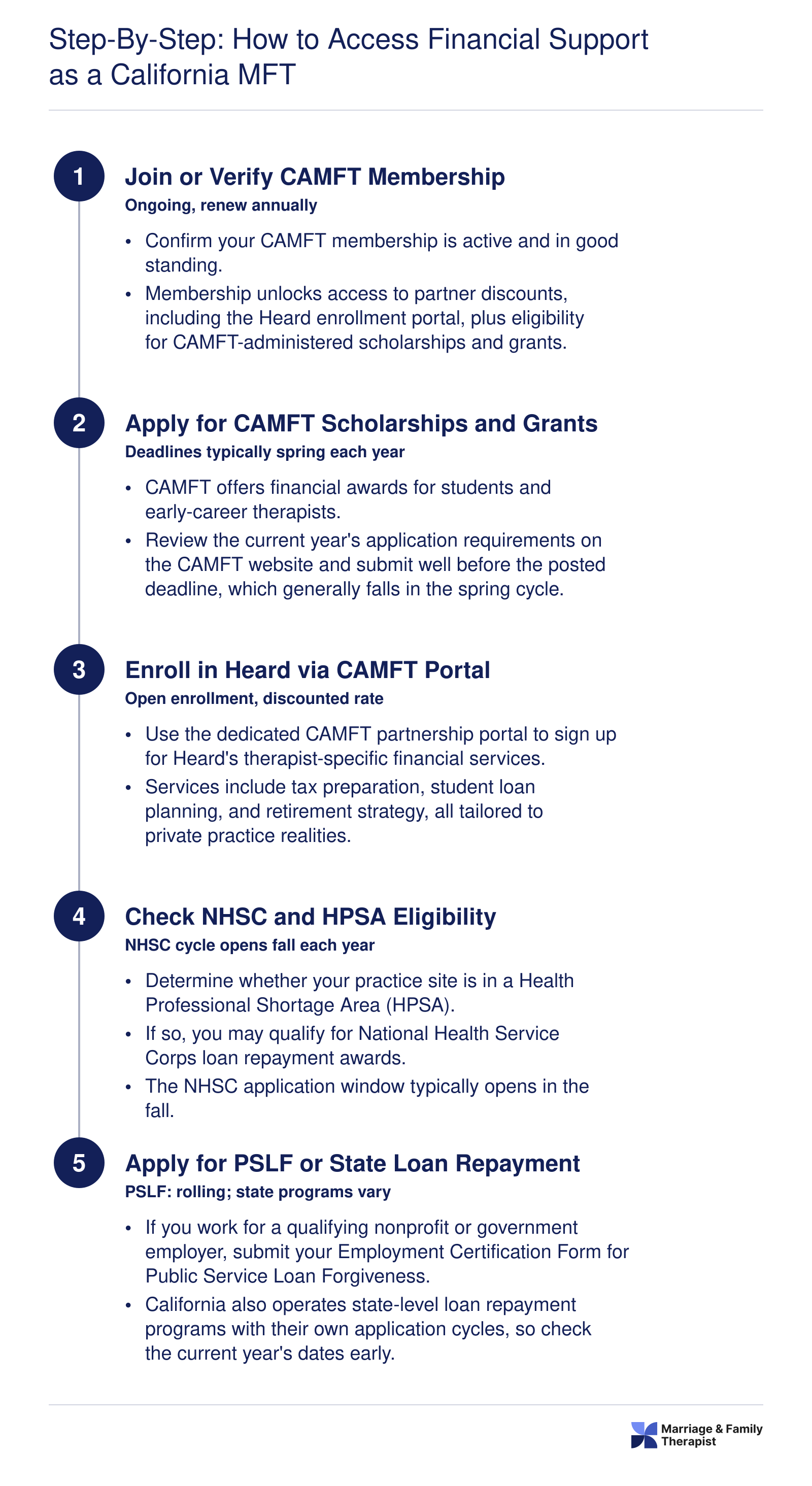

Additional Financial Support Programs for California MFTs

Award amounts up to $50,000 to $100,000 are available through the National Health Service Corps (NHSC) Loan Repayment Program for eligible mental health professionals, including LMFTs who commit to serving in designated Health Professional Shortage Areas. Beyond the Heard-CAMFT partnership, California marriage and family therapists have access to a suite of state, federal, and institutional financial support programs that can significantly reduce educational debt and offset the costs of training. These programs range from scholarship stipends that support students during their graduate training to loan repayment initiatives for practicing clinicians. Understanding the landscape of available aid, application timelines, and service commitments is essential for MFTs at every career stage.

National Health Service Corps (NHSC) Loan Repayment Program

The NHSC Loan Repayment Program targets clinicians working in underserved communities and has expanded eligibility to include licensed marriage and family therapists in recent years. LMFTs who practice in NHSC-approved sites, such as Federally Qualified Health Centers or community mental health clinics in Health Professional Shortage Areas, can apply for awards ranging from $50,000 to $100,000 in exchange for a two- or three-year service commitment. Application windows typically open each spring, and the program prioritizes clinicians in areas with the greatest need. Applicants should check the NHSC website at nhsc.hrsa.gov regularly for updates on eligibility criteria, approved service sites, and current funding availability, as details can shift annually based on federal appropriations.

California Mental Health Stipend Programs

California offers several stipend programs designed to support graduate students in mental health fields. The California Behavioral Health Scholarship Program provides awards of $25,000 to students pursuing degrees in psychiatry, psychology, clinical social work, or marriage and family therapy.1 Recipients commit to working in an underserved area or with an underserved population for a specified period after graduation, and applications are due each February.1 Additionally, CalSWEC, administered through the University of California, Berkeley, historically managed stipend programs for social work students and has expanded partnerships to include other mental health disciplines at select campuses. Students should visit the CalSWEC website at calswec.berkeley.edu and contact their university's MFT program directly to inquire about current mental health stipend offerings, which have ranged from $18,500 to $25,000 annually, and to confirm application deadlines and service requirements.

County and Federal Workforce Development Grants

Many California counties operate their own stipend and loan forgiveness programs to recruit mental health clinicians. Los Angeles County Department of Mental Health, for example, has offered training stipends and loan repayment assistance to clinicians who commit to serving county clients. Prospective applicants should explore individual county mental health department websites for eligibility details and application cycles. At the federal level, the Health Resources and Services Administration (HRSA) administers the Behavioral Health Workforce Education and Training (BHWET) grants, which fund universities and training programs to expand the mental health workforce. While BHWET funds typically flow to institutions rather than individuals, students enrolled in BHWET-supported programs may receive tuition support or stipends. Check the HRSA BHWET page at bhw.hrsa.gov for a list of current grant recipients and MFT-specific training initiatives.

Professional Association and Institutional Scholarships

In addition to government programs, California MFT students can access scholarships from professional associations and healthcare organizations. The CAMFT Educational Foundation Scholarships and Grant awarded up to $4,000 in the 2025-2026 cycle, with applications due in early November.2 Kaiser Permanente's Mental Health Scholars Academy offered a $3,000 scholarship for the 2026 cycle, with a March 3, 2026 deadline.1 HealthForce Partners provides scholarships of $5,000 to MSW, MFT, and PCC students, and the National Board for Certified Counselors (NBCC) offers Rural and Military Graduate Scholarships of $8,000 to students committed to serving military and veteran families.1 University-specific aid is also available. San Francisco State University and UCLA both maintain dedicated pages listing state grants and institutional scholarships for graduate students in mental health fields, accessible through their financial aid offices.

Public Service Loan Forgiveness for MFTs

Marriage and family therapists employed full-time by qualifying nonprofit or government agencies may be eligible for Public Service Loan Forgiveness (PSLF), which forgives the remaining balance on federal Direct Loans after 120 qualifying monthly payments under an income-driven repayment plan. Clinicians pursuing California LMFT licensing who work in community mental health centers, public schools, or nonprofit hospitals should confirm their employer's PSLF eligibility and enroll in an income-driven repayment plan as early as possible. PSLF does not require upfront application fees or service in a specific geographic area, making it a versatile option for MFTs in diverse practice settings.