Most MFTs recoup their total degree investment within 4 to 8 years of reaching full licensure.

Private practice MFTs can earn $90,000 to over $150,000 annually, roughly double typical agency salaries.

BLS projects 13% job growth for MFTs from 2024 to 2034, more than four times the national average.

Choosing a public or online program over a private university can cut total degree costs by $40,000 or more.

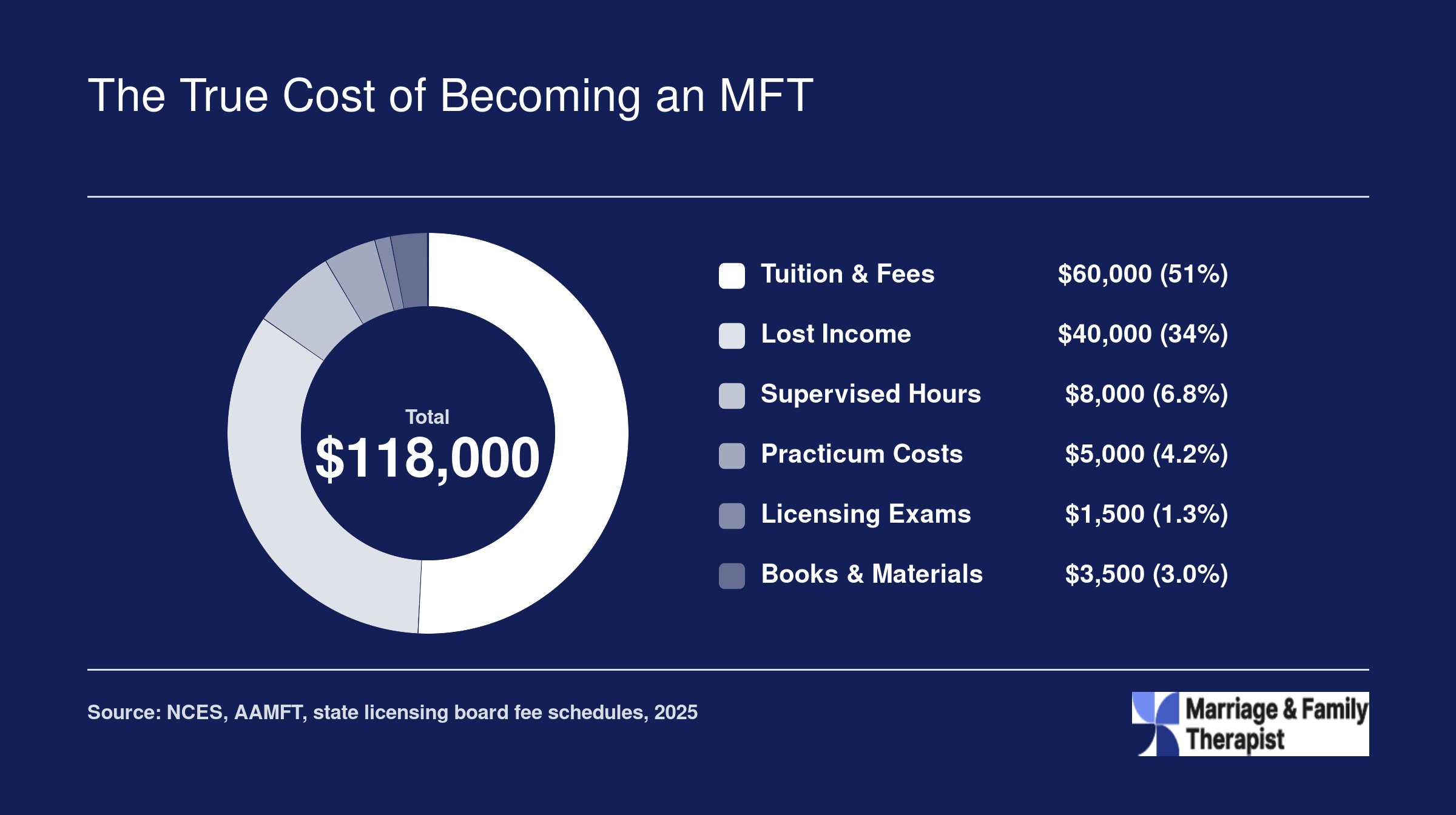

A COAMFTE-accredited master's in marriage and family therapy typically costs between $30,000 and $120,000, depending on whether you attend a public university or a private program. Add two to three years of supervised post-graduate hours at associate-level pay, and the total financial commitment before full licensure can stretch well beyond the sticker price of tuition alone.

MFT work carries genuine personal rewards, but personal fulfillment does not retire student loans. The financial question deserves its own analysis, separate from the emotional one. What follows is a breakdown of real costs, state-by-state salary data, break-even timelines, side-by-side degree comparisons, and concrete strategies to tilt the math in your favor.

With BLS projections showing 13% job growth for MFTs through 2034 and median salaries varying by more than $30,000 depending on state and practice setting, the ROI picture is not uniform. It depends almost entirely on the choices you make before, during, and after your program. Understanding whether LMFT licensure is necessary for your career is one of those early decisions that shapes everything that follows.

How Much Does an MFT Degree Actually Cost?

Before you can calculate whether an MFT degree is worth the investment, you need an honest accounting of what that investment actually looks like. Tuition is the headline number, but it is far from the only expense you will face on the path to licensure.

Tuition by Program Type

MFT master's programs span a wide price range depending on institution type and residency status. Here is what you can realistically expect to pay for the full program (typically two to three years of coursework):

Public in-state: $18,000 to $32,000. This is the most affordable route. CSU East Bay, for example, runs roughly $14,350 for in-state students.

Public out-of-state: $40,000 to $55,000. Crossing state lines for a public university nearly doubles your bill.2

Private nonprofit: $60,000 to $80,000 or more. Prestigious programs like those at Loyola Marymount (about $83,100) and Pepperdine's evening format (about $85,500) land squarely in this range, while the University of San Diego tops $93,000.

Online and low-residency: $25,000 to $90,000. The spread here is enormous. Public online programs can stay below $50,000, while private online options, such as Pepperdine's online MFT program at roughly $105,400, rival or exceed on-campus private tuition.

If cost is a primary concern, our directory of affordable online MFT programs is a good starting point for narrowing your search.

The Hidden Costs Competitors Leave Out

Tuition tells only part of the story. Several additional expenses accumulate quietly over the course of your degree and pre-licensure period:

Practicum and clinical placement fees: Many programs charge semester-based clinical training fees on top of standard tuition, sometimes $500 to $1,500 per term.

Individual supervision: Post-graduation supervision toward licensure can cost $75 to $150 per session, adding thousands of dollars before you sit for your licensing exam.

Professional liability insurance: Required during clinical placements and beyond, typically $150 to $300 per year for a student policy.

Background checks and application fees: State licensing boards, clinical sites, and exam registrations each carry their own fees.

Lost income: Perhaps the largest hidden cost. Two to three years of full-time study means forgoing tens of thousands of dollars in potential earnings, a factor that dramatically raises the true price tag.

Average Student Loan Debt

Survey data on MFT and counseling master's graduates shows that median total educational debt at graduation typically falls between $40,000 and $80,000, with total student loan balances (including any undergraduate borrowing) reaching $50,000 to $100,000 for many graduates.2 Public in-state students tend to land on the lower end, often graduating with $15,000 to $40,000 in graduate-specific debt, while private school graduates frequently carry $40,000 to $80,000 or more from the master's program alone.

Why Accreditation Affects Long-Term Value

Programs accredited by COAMFTE or CACREP sometimes carry higher tuition than unaccredited alternatives, but this premium can pay for itself over time. Graduates of accredited programs typically enjoy smoother licensure portability when moving between states, broader insurance panel acceptance, and stronger employer recognition. For a closer look at what the full LMFT licensing requirements involve, consult our licensing guide. If you plan to relocate or eventually open a private practice across state lines, accreditation is less of a cost and more of a strategic investment in your career flexibility.

The bottom line: total out-of-pocket spending for an MFT degree, including tuition, fees, supervision, insurance, and opportunity cost, can range from under $40,000 for a frugal in-state path to well over $150,000 at a high-tuition private institution. Knowing your real number is the essential first step in determining your personal return on investment.

The True Cost of Becoming an MFT

Tuition is the headline number, but it is far from the only expense. When you map out every dollar between enrollment and full licensure, a clearer picture emerges of where your investment actually goes. Understanding each component helps you plan smarter and avoid surprises.

MFT Salary Expectations by State and Setting

Where you practice has a significant impact on your earning potential as a marriage and family therapist. The table below shows median and mean annual wages for MFTs across 25 states, based on the latest Bureau of Labor Statistics data. States with higher costs of living tend to offer larger salaries, but the spread between the 25th and 75th percentile within each state reveals just how much setting, experience, and specialization can move the needle.

State

Total Employed

25th Percentile

Median Salary

Mean Salary

75th Percentile

New Jersey

3,940

$77,380

$89,030

$91,980

$97,670

Utah

1,980

$63,220

$81,170

$85,550

$102,810

Virginia

910

$54,010

$80,670

$78,900

$95,120

Oregon

1,080

$65,400

$79,890

$94,520

$137,950

Connecticut

390

$59,000

$76,930

$94,830

$138,610

Minnesota

3,780

$59,720

$72,370

$72,900

$82,870

Colorado

810

$54,960

$69,990

$89,280

$104,990

Nebraska

50

$46,040

$68,550

$68,000

$79,710

New Mexico

250

$57,800

$67,990

$68,660

$76,070

Kansas

160

$56,150

$66,620

$63,480

$68,030

Maryland

340

$58,560

$65,300

$84,900

$113,800

New York

930

$54,120

$65,020

$66,710

$76,920

Missouri

530

$51,310

$64,900

$70,010

$80,760

Pennsylvania

2,360

$55,580

$64,570

$67,940

$80,100

Ohio

710

$41,600

$63,880

$78,300

$96,220

California

32,070

$47,730

$63,780

$74,660

$91,660

Delaware

380

$53,560

$63,360

$64,840

$76,350

Massachusetts

530

$56,720

$62,290

$68,430

$81,810

Alaska

80

$48,480

$62,220

$69,970

$75,560

Iowa

90

$49,460

$61,450

$72,070

$71,030

Vermont

110

$55,310

$61,060

$66,260

$72,360

Kentucky

410

$43,020

$60,190

$65,100

$84,290

Illinois

840

$54,340

$60,140

$66,640

$71,190

Washington

N/A

$57,100

$59,660

$68,250

$70,710

Maine

N/A

$67,720

$68,670

$72,820

$85,370

Questions to Ask Yourself

Are you planning to practice in a high-paying state like California or New Jersey, or in a lower-paying rural market?

Where you practice can swing your annual earnings by $20,000 or more. If you are committed to a lower-paying region, your break-even timeline stretches significantly, making tuition costs and loan terms even more critical to evaluate upfront.

Would you be comfortable earning agency-level income for three to five years while building toward private practice?

Most new MFTs start in agency or community mental health roles at modest salaries before transitioning to higher-paying private practice. If that initial income gap would cause serious financial strain, factor post-licensure debt payments into your plan now.

Is geographic flexibility part of your career plan, and does licensure portability matter to your timeline?

Some states have complex reciprocity rules that can delay your ability to practice after a move. If relocation is likely, choosing a COAMFTE-accredited program and targeting states with streamlined portability can save you months of lost income.

Top-Paying Metro Areas for Marriage and Family Therapists

Location has a significant impact on MFT earning potential. The table below ranks the highest-paying metropolitan areas for marriage and family therapists based on federal wage data. California dominates the list, but several metros outside the state offer competitive salaries, especially when adjusted for cost of living. If maximizing your MFT degree ROI is a priority, targeting your career in one of these regions can meaningfully shorten your break-even timeline.

Metro Area

Total MFTs Employed

Mean Annual Salary

Median Annual Salary

25th Percentile

75th Percentile

Portland, Vancouver, Hillsboro (OR/WA)

700

$97,600

$84,810

$65,400

$137,950

San Jose, Sunnyvale, Santa Clara (CA)

1,220

$96,000

$88,950

$59,560

$123,430

San Francisco, Oakland, Fremont (CA)

3,400

$88,320

$76,980

$57,980

$104,970

New York, Newark, Jersey City (NY/NJ)

2,900

$83,840

$86,120

$70,660

$97,670

Salt Lake City, Murray (UT)

760

$81,560

$81,170

$60,780

$95,570

Sacramento, Roseville, Folsom (CA)

1,270

$79,940

$72,810

$49,010

$96,480

Philadelphia, Camden, Wilmington (PA/NJ/DE/MD)

2,060

$78,740

$80,090

$62,830

$89,030

Fresno (CA)

680

$74,030

$66,090

$43,480

$92,630

Los Angeles, Long Beach, Anaheim (CA)

12,400

$73,400

$64,420

$47,050

$91,580

Minneapolis, St. Paul, Bloomington (MN/WI)

2,490

$73,370

$72,910

$59,780

$83,830

Oxnard, Thousand Oaks, Ventura (CA)

1,010

$71,040

$49,280

$43,730

$66,130

Riverside, San Bernardino, Ontario (CA)

2,200

$69,670

$60,780

$45,260

$79,030

Chicago, Naperville, Elgin (IL/IN)

710

$68,190

$60,580

$58,040

$71,190

San Diego, Chula Vista, Carlsbad (CA)

4,660

$64,610

$48,950

$48,950

$75,750

Nashville, Davidson, Murfreesboro, Franklin (TN)

950

$47,570

$47,060

$40,750

$49,950

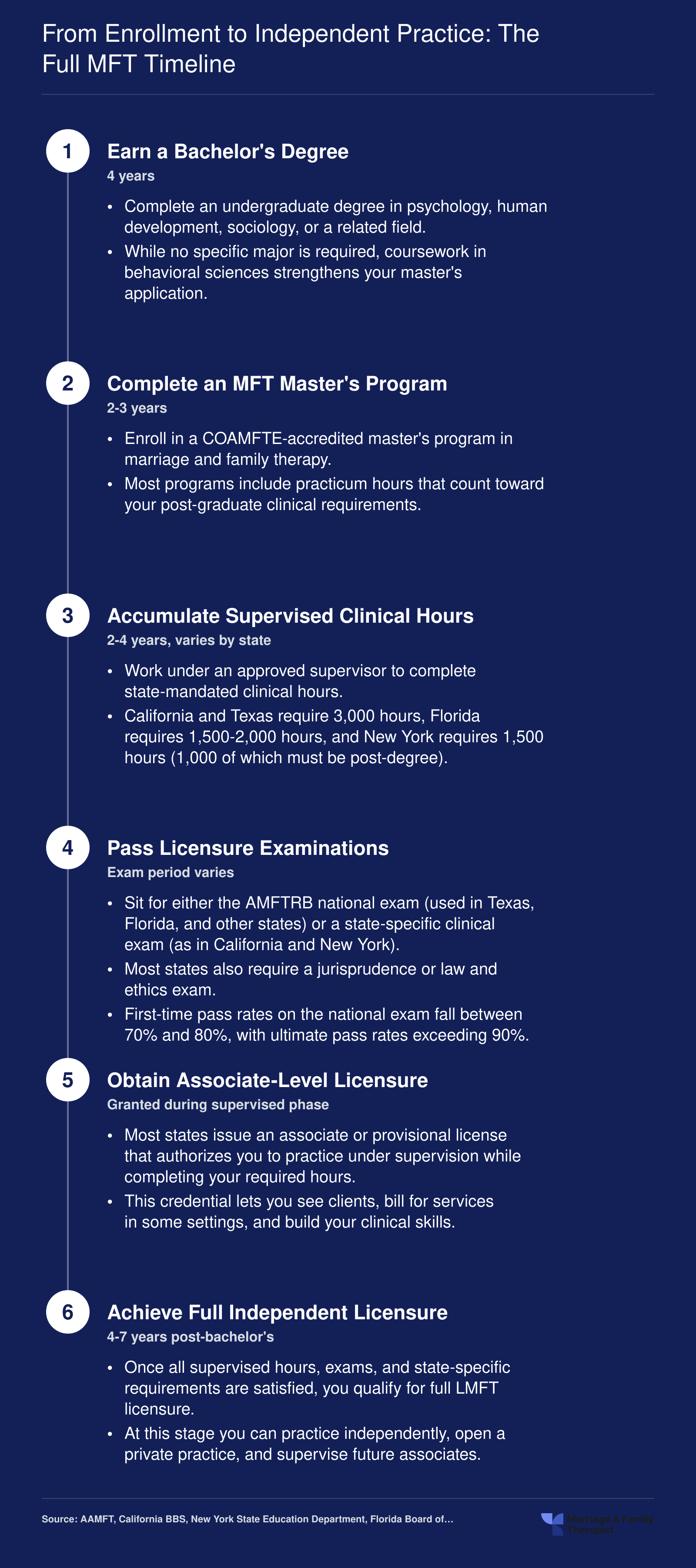

From Enrollment to Independent Practice: The Full MFT Timeline

The path from first-time college student to fully licensed marriage and family therapist is a structured sequence that typically spans 7-10 years, or 4-6 years if you already hold a bachelor's degree. Your state of practice plays a major role in how long the post-graduate phase takes, with supervised hour requirements ranging from 1,500 in New York to 3,000 in California and Texas.

Break-Even Timeline: When Does an MFT Degree Pay for Itself?

One of the most practical ways to evaluate whether an MFT degree is worth the money is to calculate how long it takes for your increased earnings to recoup your educational investment. The answer depends on three variables: how much you spent on your degree, how much you would have earned without it, and how quickly you reach full licensure and beyond.

Three Break-Even Scenarios

Using the BLS median salary for marriage and family therapists (roughly $58,000 nationally) and subtracting a baseline salary of approximately $35,000 to $40,000 for positions typically available without a graduate degree, the annual earnings advantage of holding an MFT license lands in the range of $18,000 to $23,000 per year. For a closer look at compensation benchmarks, see our marriage and family therapy salary breakdown. Applied against common debt loads, the math looks like this:

$50,000 in total debt: Break-even in roughly 2.5 to 3 years of full-time licensed practice.

$75,000 in total debt: Break-even in approximately 3.5 to 4.5 years of licensed practice.

$100,000 in total debt: Break-even in roughly 5 to 6 years of licensed practice.

These estimates assume you are making standard loan payments and that your living expenses remain relatively stable compared to your pre-degree baseline.

The Associate-Level Pay Gap

What the simple math above does not capture is the supervised clinical period required before full licensure. In most states, new graduates spend two to three years accumulating supervised hours as associate-level therapists, and pay during this stage is often meaningfully lower than the median for fully licensed MFTs. Salaries for associates commonly range from $38,000 to $48,000 depending on the employer and state. Our guide to the difference between AMFT and LMFT explains how these designations affect both scope of practice and compensation. That narrower gap between your pre-degree earnings and your associate salary means the first few years post-graduation contribute less toward your break-even point than the years that follow.

How Private Practice Changes the Equation

Once you hold a full license and transition into private practice, earning potential jumps considerably. Therapists in private practice routinely earn $80,000 to $120,000 or more, depending on caseload, specialization, and location. At that income level, the annual earnings advantage over a no-degree baseline widens to $40,000 to $85,000, and the break-even timeline compresses dramatically. Many private-practice MFTs fully recoup their educational investment within five to eight years of obtaining licensure, even on higher debt loads.

Cutting Years Off the Timeline

Program selection has an outsized effect on when you break even. Choosing a public, in-state, or accredited online program can reduce total degree costs by $30,000 to $50,000 compared to a private university. That difference alone can shave two to three years off your payback period. Comparing best online MFT programs 2025 side by side is one of the fastest ways to identify cost-effective options. Pairing a lower-cost program with employer tuition assistance, scholarships, or income-driven repayment plans during the associate phase further accelerates the return. The bottom line: the less you borrow, the sooner your degree starts generating net positive returns, and the sooner you can redirect those earnings toward building the career and life you want.

MFT vs MSW vs LPC: Comparing the ROI of Therapy Degrees

If you are weighing a master's degree in marriage and family therapy against a Master of Social Work (MSW, leading to LCSW licensure) or a clinical mental health counseling degree (leading to LPC or LCPC licensure), the return on investment differs in ways that go well beyond sticker price. All three credentials qualify you to practice therapy, but the financial calculus depends on program cost, earning potential, job market breadth, and how quickly you can build the career you want.

Program Cost Comparison

Total tuition and fees for each pathway in 2026 fall into overlapping but distinct ranges:

MFT (LMFT): $25,000 to $70,000

MSW (LCSW track): $20,000 to $60,000

LPC/LCPC: $25,000 to $65,000

MSW programs tend to sit at the lower end because many large public universities operate well-established social work schools with strong funding pipelines. MFT programs sometimes skew higher because fewer institutions offer COAMFTE-accredited degrees, which limits competition on price. That said, affordable options exist for every path if you prioritize in-state public programs or competitively priced online formats.

Post-Licensure Salary Ranges

Median salaries after full licensure also overlap, though LCSWs currently edge ahead at the top:2

LMFT: $55,000 to $75,000

LCSW: $60,000 to $80,000

LPC/LCPC: $58,000 to $78,000

The LCSW advantage stems partly from a broader scope of practice that includes case management, hospital social work, and administrative roles in addition to clinical therapy. LMFTs and LPCs can close that gap, especially in private practice settings where reimbursement is tied to session volume rather than title.

Licensure Portability and Job Market Breadth

This is where the three credentials diverge most sharply. Social work licensure (LCSW) is recognized in all 50 states with a relatively consistent set of requirements, making it the most portable of the three. LPC licensure has improved in portability in recent years thanks to interstate compact efforts, though requirements still vary. LMFT licensure carries its own interstate compact movement, but the number of participating states remains smaller as of 2026.

Job market breadth also favors the LCSW. Social workers fill roles in hospitals, schools, government agencies, nonprofits, and private practice. MFTs occupy a more specialized niche, which can be a strength (less competition for couples and family-focused positions) or a limitation (fewer agency job postings). LPCs land somewhere in the middle, with strong demand in community mental health settings and growing insurance panel acceptance.

Which Credential Offers the Best ROI?

There is no single winner. The best return depends on your goals:

If you want the widest employment options and easiest geographic mobility, the MSW-to-LCSW path typically offers the strongest financial safety net.

If you are drawn specifically to relational and systemic therapy, and especially if you plan to build a private practice in a state with strong MFT recognition (like California or New York), an MFT degree can match or exceed the ROI of the other two.

If you want flexibility between clinical work and counseling specialties such as addiction or career counseling, the LPC path strikes a practical balance.

All three degrees lead to financially viable careers in therapy. The differences lie in how quickly you recoup your investment and how much flexibility you have in shaping where and how you practice. You can compare MFT program comparison chart options alongside state-specific licensing rules and local job market conditions, which will do more to clarify your personal ROI than national averages alone.

The Bureau of Labor Statistics projects that employment for marriage and family therapists will grow 13% from 2024 to 2034, more than four times the 3.1% average projected across all occupations. That pace signals strong, sustained demand for MFTs throughout your career.

Private Practice vs Agency Work: Long-Term Earning Potential

The choice between agency employment and private practice is one of the most consequential financial decisions you will make as a licensed MFT. Each path offers a distinct income trajectory, and understanding the realistic numbers behind both options is essential to evaluating your long-term return on investment.

Agency Work: Stability With a Ceiling

Community mental health agencies, hospitals, and nonprofit organizations provide a reliable starting point. You can expect a salary range of roughly $50,000 to $70,000, along with employer-sponsored health insurance, retirement contributions, and paid time off. These benefits carry real monetary value, often adding 20 to 30 percent on top of base pay. However, agency salaries tend to plateau relatively quickly. Annual raises are modest, and moving beyond $70,000 usually requires shifting into supervisory or administrative roles, which means spending less time doing clinical work.

Private Practice: Higher Ceiling, Longer Ramp-Up

Private practice is where MFT earning potential expands dramatically, but it takes time. Here is a realistic look at the math.

In high-cost metro areas, commercial insurance reimburses licensed MFTs between $100 and $140 per session.1 Mid-range markets typically pay $80 to $110, while rural areas fall in the $65 to $90 range.1 Using a moderate estimate of $110 per session, a therapist seeing 22 clients per week across 48 working weeks would gross approximately $116,160 per year. After subtracting overhead costs of 30 to 40 percent (covering office rent, liability insurance, billing services, and marketing), net income lands between $70,000 and $81,000. Scale that caseload up to 25 sessions per week, or practice in a higher-reimbursement metro, and net income can climb above $100,000 and potentially reach $150,000 or more with a cash-pay or specialized niche.

The catch: building a full caseload typically takes two to four years post-licensure. During that ramp-up period, many therapists work part-time in an agency while growing their private caseload on evenings and weekends. Exploring various MFT career paths can help you identify the clinical specialties that command premium rates.

The Insurance Panel Factor: A Real ROI Consideration

One financial headwind that MFTs face more acutely than their LCSW counterparts involves insurance panel acceptance. Data from recent surveys show that only about 40 to 60 percent of commercial insurers readily credential LMFTs, compared to 60 to 75 percent for LCSWs.2 Medicaid participation rates tell a similar story, with MFTs accepted at roughly 20 to 40 percent versus 30 to 50 percent for social workers.2

This gap matters because fewer panel slots mean fewer insured clients flowing into your practice. The good news is that mental health parity laws continue to improve access. Medicare now reimburses MFTs directly (at about $113.90 for a standard therapy session and $167.00 for an extended session as of 2026), a milestone that has opened a large new patient pool.3 Still, about one-third of private practice therapists across all license types choose not to accept insurance at all, opting instead for private-pay models that can command $150 to $250 or more per session.2

Mapping Your Strategy

When projecting your personal ROI, consider these factors:

Agency path: Reliable income from day one, benefits included, but limited upside beyond $70,000 without a role change.

Private practice path: Net income of $80,000 to $150,000 or more is achievable, but plan for a two-to-four-year runway of lower earnings while building your caseload.

Panel access: Research insurer credentialing policies in your state before committing to an insurance-based practice model. If panel access is limited, a private-pay or hybrid model may be more realistic.

Hybrid approach: Many successful MFTs maintain a part-time agency position for steady income and benefits while scaling a private practice on the side, minimizing financial risk during the transition.

The bottom line is straightforward. Agency work offers a faster, more predictable payoff on your degree investment. Private practice offers a higher lifetime return, but only if you plan for the transition period and position yourself strategically within your local insurance landscape.

Strategies to Maximize Your MFT Degree ROI

Earning your MFT degree is a significant financial commitment, but the choices you make before, during, and after your program can dramatically shift the return on that investment. These strategies can save you tens of thousands of dollars and accelerate your path to financial stability.

Leverage Public Service Loan Forgiveness

If you plan to work at a qualifying nonprofit, government agency, or community mental health center, Public Service Loan Forgiveness (PSLF) should be central to your financial plan. After 120 qualifying monthly payments (roughly 10 years) under an eligible repayment plan, your remaining federal loan balance is forgiven entirely. For MFTs who graduate with $50,000 to $100,000 in student debt, PSLF can effectively erase the bulk of that obligation. The key is enrolling in an income-driven repayment (IDR) plan from the start, which keeps your monthly payments proportional to your income during those early, lower-earning years of supervised practice. Some community mental health employers also offer tuition assistance or loan repayment stipends, so ask about these benefits during the hiring process.

Choose Your Program Strategically

Not all MFT programs deliver the same cost-to-licensure ratio. COAMFTE-accredited online MFT programs at public universities consistently offer the strongest combination of affordability, clinical training quality, and licensure preparation. Online or hybrid programs from accredited institutions can save $20,000 to $40,000 compared to private on-campus alternatives, often without sacrificing the supervised clinical hours you need. Before committing, compare net tuition (after financial aid), graduation rates, and time-to-degree across at least three to five programs. A program that costs less but takes an extra year may not actually save you money once you factor in delayed earnings.

Specialize to Command Premium Rates

Specialization is one of the most reliable income multipliers in the therapy field. Clinicians who develop expertise in high-demand niches can charge significantly more than generalist practitioners, particularly in private practice. Consider pursuing post-masters MFT certificate training in areas such as:

Sex therapy: A relatively underserved specialty with strong private-pay demand.

Trauma treatment (EMDR): Certification in evidence-based trauma modalities opens doors to both agency contracts and premium private-pay clients.

Couples intensives: Multi-hour or multi-day formats that allow you to charge $150 to $250 or more per session, with some intensive models generating considerably higher per-client revenue.

These specializations typically require post-licensure training and certification, but the investment is modest (often a few thousand dollars) relative to the income boost they produce. Building a niche reputation also reduces your dependence on insurance panels and their lower reimbursement rates.

Combine Strategies for Maximum Impact

The most financially savvy MFTs layer these approaches. They attend an affordable, well-accredited program, use IDR plans while accumulating supervised hours at a qualifying employer, pursue PSLF to eliminate remaining debt, and then transition into specialized private practice once licensed. This sequence minimizes out-of-pocket costs during the years when your earning power is lowest and positions you for the highest possible income once you have full clinical independence. Understanding the broader marriage and family therapy career outlook helps you plan this trajectory with the same intentionality you bring to your clinical training, which is what separates therapists who thrive from those who feel trapped by their student debt.

The return on an MFT degree hinges on two variables you can control: what you pay for the degree and how you practice after licensure. A public or online program paired with a deliberate path toward private practice can break even in roughly five to eight years and reach six figures within a decade. The same credential from a high cost private institution, followed by agency only employment in a low paying state, may never fully recoup the investment. Choose both sides of the equation carefully.

Is an MFT Degree Worth It? The Bottom Line

After weighing the costs, timelines, salary data, and earning trajectories covered throughout this guide, the answer is clear: yes, an MFT degree is worth the financial investment, provided you manage three critical variables well.

The Three Variables That Determine Your ROI

Every MFT candidate's return on investment hinges on the same trio of decisions.

Program cost: Choosing a COAMFTE-accredited program at a public university or pursuing assistantship-funded tuition can cut your total investment by half or more compared to premium private institutions. Keeping total student debt below your realistic first-year salary is the single most important financial guardrail you can set.

Geographic market: States and metro areas with higher demand, insurance-friendly licensing structures, and mid-to-high cost-of-living indices consistently produce stronger MFT salaries. California, New Jersey, and several East Coast metros stand out, but even moderate-cost regions can deliver solid returns when demand outpaces supply.

Career setting: Agency and community mental health roles offer stability and often loan-forgiveness eligibility, yet private practice remains the primary path to top-tier earnings. Therapists who build a private caseload in a favorable market are the ones most likely to cross the six-figure threshold.

Can MFTs Really Earn Six Figures?

Yes, MFTs can and do earn $100,000 or more, but that outcome is neither automatic nor immediate. Six-figure incomes are concentrated among clinicians in private practice who serve mid-to-high-cost markets, carry a full or near-full caseload, and often layer in specialized services such as couples intensives or clinical supervision. Most therapists who reach that level do so roughly five to eight years after completing their degree, once they have accumulated marriage and family therapy internship hours, built referral networks, and refined a niche. Expecting that income in year one is unrealistic; planning to reach it within a decade is not.

Beyond the Spreadsheet

Financial return is only part of the picture. Marriage and family therapists consistently report high job satisfaction, citing the depth of client relationships and the ability to witness meaningful change in families. Private practice offers schedule flexibility that few salaried careers can match. And projected marriage and family therapist job outlook continues to outpace the average across all occupations, which means demand for your credential is trending in the right direction for years to come.

A Simple Decision Framework

If you want a concrete way to evaluate whether this investment makes sense for you, apply this test before you commit:

Your total anticipated student debt will be less than your expected first-year post-licensure salary in your target market.

You have a realistic, time-bound plan to transition into private practice (or a high-paying specialty role) within five years of graduation.

You are willing to be strategic about where you practice and which populations you serve.

If all three conditions hold, the math works. The MFT degree is not a gamble under those circumstances; it is a calculated career investment with a well-documented payoff. Use the salary tables, cost breakdowns, and timeline data on Marriage & Family Therapy (MFT) Resources to pressure-test your own numbers before you enroll, and you will enter your program with the confidence that the return is real.

Frequently Asked Questions About MFT Degree ROI

Below are the most common questions aspiring therapists ask when weighing the financial side of an MFT degree. Each answer draws on the salary data, cost benchmarks, and career timelines covered throughout this guide.

Is an MFT degree worth the money?

For most graduates, yes. The Bureau of Labor Statistics reports a median annual salary of roughly $58,510 for marriage and family therapists, and those who move into private practice often earn considerably more. When you factor in strong job growth projections and the relatively short path to licensure compared to doctoral programs, the long-term return on investment is favorable, especially if you manage tuition costs strategically through public universities or employer tuition assistance.

How long does it take to become a licensed MFT?

Plan for roughly five to seven years from the start of your master's program to full licensure. The degree itself typically takes two to three years. After graduation, most states require between 2,000 and 4,000 hours of supervised clinical experience, which usually takes an additional two to three years of post-degree work. Some states also require a period of supervised practice before you can sit for the licensing exam.

Can you make six figures as a marriage and family therapist?

Yes, though it generally requires building a private practice, specializing in a high-demand niche, or working in a top-paying metro area. Therapists in the top ten percent of earners surpass $96,000 annually according to federal wage data, and those operating full private-practice caseloads in high-cost markets like San Francisco, Los Angeles, or New York often cross the six-figure threshold within a few years of launching their practice.

How much does an MFT program cost?

Total tuition for a COAMFTE-accredited master's program ranges from approximately $20,000 at in-state public universities to $100,000 or more at private institutions. The median falls somewhere around $40,000 to $60,000 when you include fees and materials. Choosing a public school, securing assistantships, and applying for scholarships are the most effective ways to keep the total investment on the lower end.

Is an MFT or LCSW a better career investment?

It depends on your career goals. LCSWs tend to have broader insurance-panel access and slightly higher median salaries in agency settings, while MFTs often earn more in private practice focused on couples and family work. Job growth projections are strong for both credentials. If your passion is relational and systemic therapy, the MFT path offers a more specialized skill set that can command premium fees in private practice.

What is the job outlook for marriage and family therapists?

The Bureau of Labor Statistics projects employment for marriage and family therapists to grow roughly 15 percent through the early 2030s, which is significantly faster than the average for all occupations. Rising public awareness of mental health, expanded insurance coverage, and growing demand for telehealth services are all driving this growth. Graduates entering the field in 2026 face a favorable market with more openings than qualified candidates in many regions.