Graduate MFT students can borrow up to $20,500 per year in federal Direct Unsubsidized Loans through FAFSA.

Stacking scholarships, employer tuition assistance, and federal loans can cut a program like NDNU's $63,540 cost by half or more.

Licensed MFTs in California earn between $82,000 and $124,000 annually, strengthening the return on investment.

Public Service Loan Forgiveness can eliminate remaining federal loan balances after 120 qualifying payments in eligible settings.

What does an MFT degree actually cost after financial aid? The raw tuition numbers, anywhere from $30,000 to over $120,000, tell only part of the story. Master's programs like Notre Dame de Namur University's online MFT list a total cost of $63,540, yet most students never pay that amount. Federal Direct Unsubsidized Loans cap at $20,500 annually, AAMFT scholarships start at $1,000, and California-licensed marriage and family therapists earn between $82,000 and $124,000, making the degree an investment with measurable return. The real question is not the sticker price but how many funding layers you can stack. When institutional aid, employer reimbursement, and loan forgiveness intersect, the net price often drops below half the published figure, and that changes the affordability calculus completely.

How Much Does an MFT Degree Actually Cost?

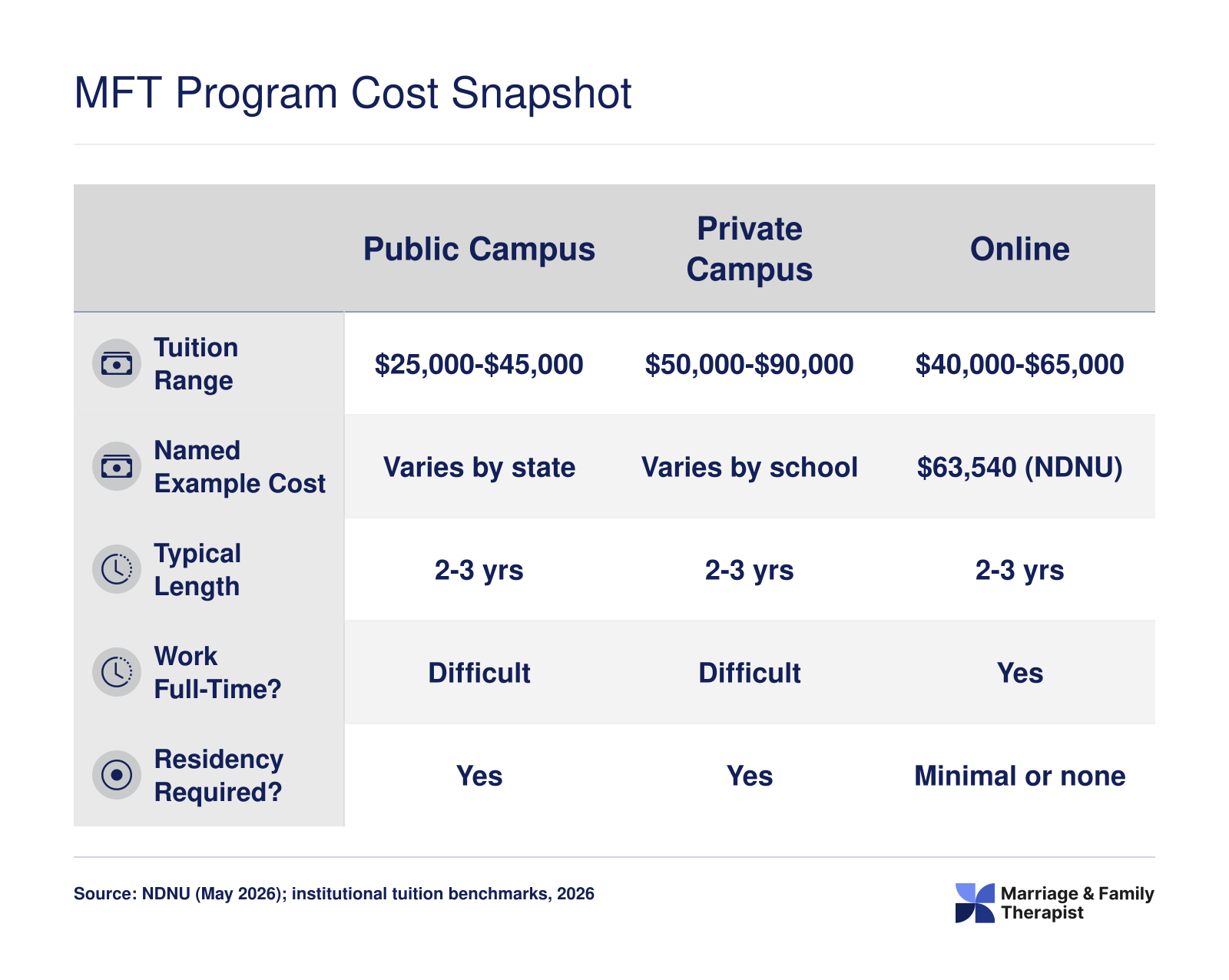

Cost and accreditation type are the two biggest variables that determine both your monthly student loan payment and your career options after graduation. Understanding these tradeoffs early helps you compare programs on a true net-price basis, not just the sticker price. For example, Notre Dame de Namur University's Master's in Clinical Psychology (MFT track) carries a total cost of $63,540 before financial aid.1 That figure is a useful benchmark, but it sits in the middle of a wide range across programs.

Tuition Pages on University Websites Are Your First Stop

Published tuition rates change annually, and the figure on a program comparison site may be a year or more out of date. Go directly to the graduate admissions or financial aid section of each school you are considering. Look for a detailed cost of attendance that includes tuition, fees, books, and estimated living expenses if you are relocating or reducing work hours. Programs delivered online may have separate tuition schedules, often charging a flat per-credit rate regardless of residency, which simplifies budgeting but sometimes excludes campus-based fee waivers. If budget is your top priority, our directory of cheapest MFT programs is a good starting point for narrowing your list.

Accreditation Shapes Your Financial Aid Package

Whether a program holds COAMFTE or CACREP accreditation can affect eligibility for federal student loans, certain institutional scholarships, and graduate assistantships. While both pathways lead to licensure in many states, financial aid offices sometimes apply different policies to each accreditation type. Contact the financial aid office at each prospective school and ask directly: *How does the program's accreditation impact my access to federal Direct Unsubsidized Loans, work-study, and need-based grants?* This conversation often reveals hidden aid opportunities, or restrictions, that are not obvious from the website alone.

Federal aid: Graduate students generally qualify for Direct Unsubsidized Loans, but institutional and state grant programs may have additional accreditation requirements.

Scholarships: Some COAMFTE-specific scholarships are available through professional networks, while CACREP programs may open doors to counseling-specific funding streams.

Professional Associations Offer Budgeting and Debt Context

Before committing to a program, check resources from the American Association for Marriage and Family Therapy (AAMFT) and CACREP. These organizations frequently publish member surveys that include average student loan debt at graduation, early-career earnings by region, and cost-of-living comparisons. Use this data to estimate your monthly loan payment relative to the licensure-track salaries in your target state. Our MFT degree ROI analysis walks through this calculation in detail. The Bureau of Labor Statistics website provides broader labor market context, including median wages for therapists in different settings, which helps you pressure-test whether your expected income can support the debt load you are considering.

A Quick Call to the Financial Aid Office Pays Off

Once you have identified one or two top-choice programs, schedule a call or appointment with a financial aid counselor. Come prepared with questions about assistantship timelines, scholarship application cycles, and whether the school participates in any loan repayment assistance programs for public-service track graduates. This proactive step often surfaces institution-specific grants or tuition discounts that are not widely advertised.

MFT Program Cost Snapshot

MFT master's programs vary widely in total cost, format, and flexibility. This side-by-side view helps you weigh the trade-offs across the three most common program types so you can match your budget and lifestyle to the right fit.

MFT Scholarships: National, State, and School-Based Awards

Scholarships reduce out-of-pocket costs without the repayment burden of loans, making them the first funding tool every prospective MFT student should pursue. Three tiers of awards exist: national professional-association scholarships, state-level MFT society grants, and institutional scholarships tied to your university or COAMFTE-accredited program. Each tier has distinct eligibility rules, application cycles, and competitive profiles, so a comprehensive search across all three maximizes your funding stack.

National Professional Association Scholarships

The American Association for Marriage and Family Therapy (AAMFT) maintains the most established scholarship portfolio for graduate students entering COAMFTE-accredited programs, with awards starting at $1,000.1 Visiting AAMFT's website directly ensures you see current eligibility criteria, award amounts, and deadlines, which typically fall in early spring for the following academic year. The AAMFT Minority Fellowship Program specifically supports students from underrepresented communities and may include stipends, mentorship, and conference travel funding. Similarly, the National Board for Certified Counselors (NBCC) Foundation offers fellowships for mental-health graduate students, including those pursuing MFT degrees, with special consideration for those committed to serving underserved populations.

The California Association of Marriage and Family Therapists (CAMFT) provides scholarships for students enrolled in California programs, though residency or program location requirements vary by award. Checking CAMFT's website directly reveals both statewide scholarships and regional chapter awards, which often have lower applicant pools and higher success rates for students in specific counties or training sites.

State and Regional MFT Association Awards

Beyond California, most states maintain their own marriage and family therapy associations that offer modest scholarships ranging from a few hundred to several thousand dollars. These state associations often prioritize members, so joining your state's MFT society as a student member (usually less than fifty dollars annually) can unlock scholarship eligibility and networking access. Contact state associations directly by phone or email if their websites lack detailed scholarship information; smaller organizations may not post formal applications online but will share details upon inquiry. State awards frequently have rolling or late-summer deadlines, allowing you to apply even after national deadlines have passed.

School-Based and COAMFTE-Linked Institutional Scholarships

Your university's financial aid office and MFT program department are critical resources for internal scholarships that do not appear on national databases. COAMFTE-accredited programs often receive philanthropic gifts earmarked for MFT students, and these awards may not be widely advertised outside the department. Some institutions, such as Notre Dame de Namur University, offer need-based scholarships specifically for MFT students from underrepresented communities.1 Schedule a meeting with your program director or financial aid counselor during your application process to ask specifically about departmental scholarships, graduate assistantships, and tuition waivers. Institutional awards may prioritize criteria such as academic merit, clinical placement performance, or commitment to specific populations like children, veterans, or LGBTQ+ communities.

Supplementing Your Search with Aggregator Tools

Scholarship aggregators like Fastweb and Scholarships.com allow you to filter by field of study, but their MFT-specific listings are often incomplete or outdated. Use these platforms as a supplement, not a replacement, for direct searches on AAMFT, NBCC, and state association websites. Always verify award details, deadlines, and application links on the official scholarship sponsor's site before investing time in an application. Generic mental-health or graduate-student scholarships listed on aggregators can still apply to MFT students, broadening your pool of opportunities beyond MFT-exclusive awards.

Questions to Ask Yourself

Are you from an underrepresented community in the therapy field?

AAMFT and institutional minority fellowships specifically support diverse candidates, reducing reliance on student loans and making MFT education more affordable for those who qualify.

Are you already working in behavioral health or community services?

Service-related scholarships and employer tuition benefits can combine, allowing you to stack multiple funding sources and significantly lower your net cost.

Would you commit to a post-graduation placement in an underserved area?

Loan repayment and scholarship-for-service programs trade tuition dollars for years of service, often wiping out tens of thousands in debt while filling critical workforce gaps.

Federal Financial Aid for MFT Graduate Students

Federal student aid for graduate students operates on different rules than undergrad funding, and understanding those rules before you borrow can save you thousands over the life of your loans.

Filing FAFSA as a Graduate Student

Graduate students are treated as independent for federal aid purposes, which means your parents' income does not factor into your eligibility. You fill out the FAFSA based solely on your own financial information. Filing as early as possible matters: some aid programs have limited funds and award on a first-come, first-served basis, even when federal loan limits are fixed. The FAFSA opens each October for the following academic year, so aim to submit in October or November rather than waiting until spring.

One important checkpoint: federal aid is only available at institutions that participate in Title IV programs. For MFT students, this makes accreditation a practical financial concern, not just an academic one. Programs holding COAMFTE accreditation or CACREP accreditation tend to meet institutional eligibility standards, but you should confirm directly with any school you are considering that its MFT program qualifies students for federal aid before you apply.

Direct Unsubsidized Loans vs. Grad PLUS Loans

Graduate students can access two primary federal loan types, and the order in which you borrow matters.

Direct Unsubsidized Loans: Capped at $20,500 per academic year, these loans carry a fixed interest rate set annually by Congress (currently lower than Grad PLUS rates).1 Interest accrues while you are in school, but the rate is more favorable than what you will find with Grad PLUS.

Grad PLUS Loans: These can cover up to your full cost of attendance minus any other aid you receive. The interest rate is higher than Direct Unsubsidized Loans, and there is a loan origination fee. They require a basic credit check.

The practical guidance: borrow Direct Unsubsidized funds first, up to the annual cap, and turn to Grad PLUS only for remaining gaps. Using both strategically means you minimize the amount sitting at the higher rate.

Does Winning a Scholarship Reduce Your Federal Aid?

This concern comes up often, and the answer is mostly good news. Scholarships count against your total cost of attendance, which is the ceiling your aid package cannot exceed. In practice, an institutional scholarship almost always reduces the amount you need to borrow rather than displacing grant aid you already hold. If a school offers you a $5,000 scholarship, your loan eligibility simply decreases by that amount. You borrow less, which is the outcome you want. The only scenario where a scholarship can displace other aid is if your total aid package already equals your full cost of attendance, a rare position for most graduate students. Applying for every scholarship available is almost always worth the time.

Loan Forgiveness and Service-Obligation Programs for LMFTs

Federal and state loan forgiveness programs can significantly reduce the net cost of an MFT degree, but they require strategic planning and a willingness to meet specific employment and service obligations. These programs are particularly valuable for graduates carrying federal student loans who plan to work in nonprofit, government, or underserved settings.

Public Service Loan Forgiveness (PSLF)

LMFTs working full-time (at least 30 hours per week) for qualifying employers can have their remaining federal Direct Loan balance forgiven after making 120 qualifying monthly payments under an income-driven repayment (IDR) plan.1 Qualifying employers include government agencies at any level and 501(c)(3) nonprofit organizations, which covers many community mental health centers, nonprofit hospitals, and family service agencies where LMFTs commonly practice.

Only Direct Loans are eligible (Direct Stafford, Direct Grad PLUS, and Direct Consolidation Loans). Payments must be made under an IDR plan such as Income-Based Repayment (IBR), Pay As You Earn (PAYE), Income-Contingent Repayment (ICR), or the newer SAVE plan, or under the standard 10-year repayment plan. The forgiven balance is not taxed at the federal level.1 Starting July 1, 2026, employers with a substantial illegal purpose may be disqualified, and the Repayment Assistance Plan (RAP) will replace IDR for certain new consolidations, so prospective applicants should verify current program rules.2

NHSC Student Loan Repayment Program

The National Health Service Corps (NHSC) Loan Repayment Program became available to Licensed Marriage and Family Therapists in recent years, yet it remains underutilized by the profession. LMFTs who commit to a minimum two-year service obligation at an NHSC-approved site in a designated Health Professional Shortage Area (HPSA) can receive between $50,000 and $75,000 in loan repayment assistance as of 2026.3 Full-time participants (40 hours per week) receive the maximum award, while part-time participants (minimum 20 hours per week) receive a reduced amount.

Applicants must be U.S. citizens or nationals and work at an approved service site, which may include Federally Qualified Health Centers (FQHCs), rural health clinics, or nonprofit mental health centers serving underserved populations. Continuation awards are available in one-year increments for those who extend their service commitment.3 This program is especially attractive for new graduates willing to begin their post-licensure career in a HPSA, as the award can eliminate a substantial portion of graduate debt while building supervised clinical experience.

State-Level Loan Repayment Programs

Many states operate their own behavioral health workforce loan repayment programs that include LMFTs, though availability and award amounts vary significantly. California, for example, has funded Mental Health Services Act (MHSA) workforce programs that provide loan repayment assistance to clinicians serving in public mental health systems. Other states with active programs include Oregon, Washington, and New York, each with distinct eligibility criteria tied to practice location, employer type, or population served.

Prospective MFT students should research their intended practice state's health workforce development office or behavioral health authority to identify current programs. Some state programs require a specific number of years of service in designated shortage areas or with underserved populations, while others offer smaller awards with shorter commitments.

Scholarship-for-Service Tradeoffs

Some programs, including the NHSC Scholars Program, cover tuition and fees in exchange for a multi-year service commitment in an underserved area. While these programs eliminate tuition debt, they lock recipients into specific practice settings and geographic locations for several years post-graduation. This is both a financial and a career decision. Prospective students should carefully consider whether the practice setting, patient population, and location align with their long-term career goals before committing to a scholarship-for-service program. For a broader look at whether total program costs justify long-term earnings, see our return on investment MFT degree analysis. For students already planning to work in underserved communities, these programs offer an excellent path to a debt-free MFT degree.

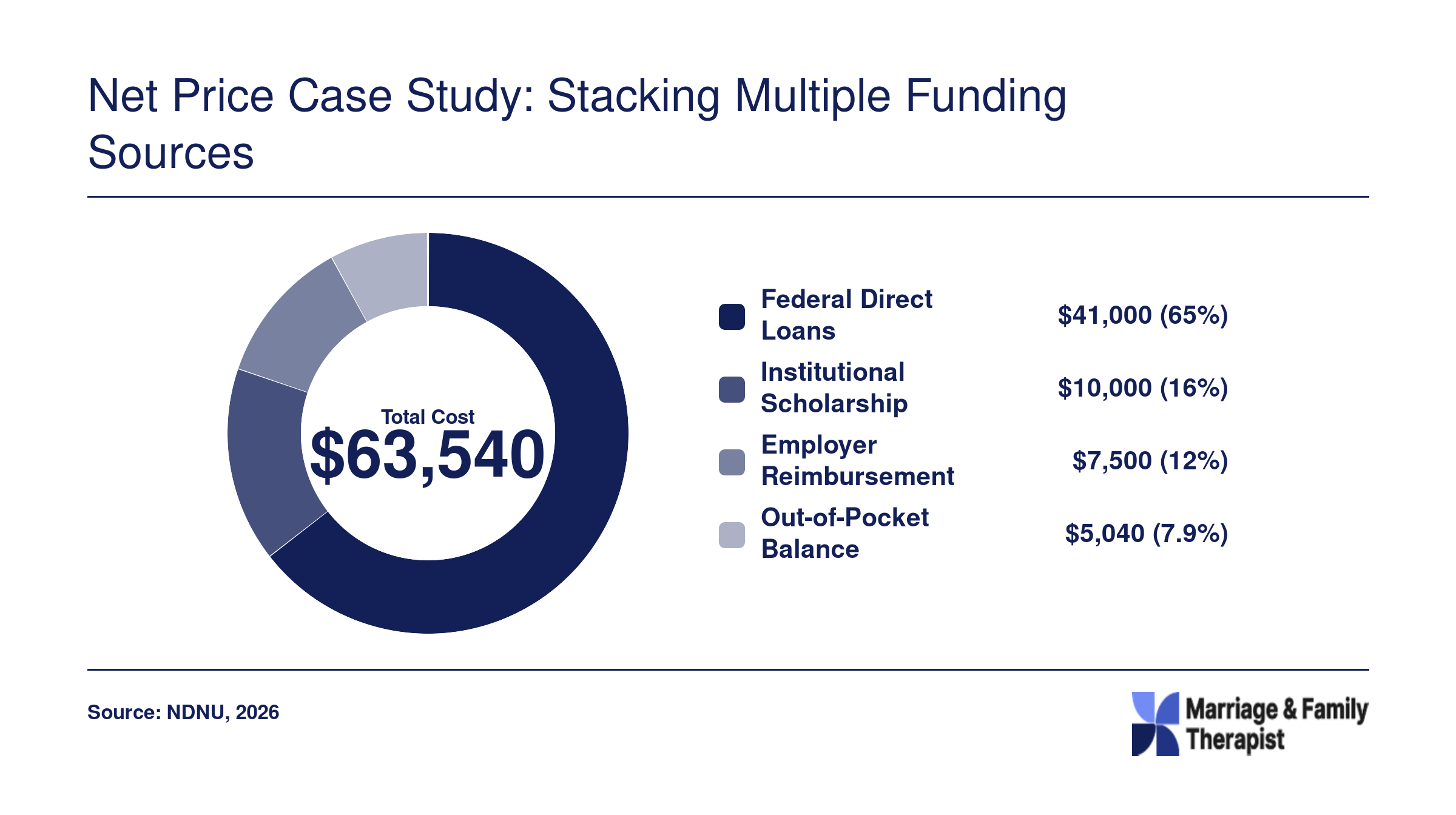

Net Price Case Study: Stacking Multiple Funding Sources

Affording an MFT degree becomes far more manageable when you layer several funding sources on top of each other. The hypothetical breakdown below uses NDNU's $63,540 total program cost as a benchmark and shows how a student who secures a modest institutional scholarship, maximizes federal Direct Unsubsidized Loans across the program, and taps an employer tuition reimbursement benefit can shrink out-of-pocket costs to a fraction of the sticker price.

Employer Tuition Assistance and Workplace Benefits for MFT Students

Employer tuition assistance is a workplace benefit in which your employer pays for some or all of your graduate school costs, often in exchange for continued employment and satisfactory academic performance. If you are already working in behavioral health, education, or healthcare, this benefit can shave thousands of dollars off your MFT degree each year, and it is more widely available than many students realize.

The Section 127 Tax Advantage

Under Section 127 of the Internal Revenue Code, employers can reimburse up to $5,250 per year in tuition expenses tax-free. That means neither you nor your employer owes federal income tax on that amount. Many behavioral health agencies, hospitals, school districts, and community mental health centers offer this benefit as part of their standard compensation packages. Over a two- or three-year master's program, $5,250 annually adds up to $10,500 to $15,750 in tuition support before you even touch loans or scholarships.

Common Employer Conditions to Watch For

Tuition reimbursement rarely comes without strings. Employers typically attach conditions such as:

Continued employment: You may need to remain with the organization for a set period after completing your degree, sometimes one to three years.

Minimum grades: Many employers require a B average or higher each term to qualify for reimbursement.

Degree relevance: The program you enroll in generally must relate to your current role or a role the employer needs to fill.

As Notre Dame de Namur University noted in a May 2026 overview of MFT affordability strategies, these requirements are standard, so it pays to read the fine print before committing to a program.1

Why Online MFT Programs Amplify This Benefit

Asynchronous online MFT programs exist precisely so students can hold down full-time jobs while earning their degree. This is not just a scheduling convenience; it is a financial strategy. If you maintain full-time employment throughout your program, you remain eligible for tuition reimbursement every year and continue earning a salary. NDNU's online MFT program, for example, uses asynchronous coursework specifically designed around working professionals' schedules, keeping the employer benefit pipeline open from enrollment through graduation.1

Additional Workplace Perks at Community Mental Health Centers

Some community mental health employers go beyond the standard $5,250 reimbursement. Certain agencies offer supplemental tuition grants, reduced-cost supervision hours, or the ability to count employment hours toward practicum requirements. If you are weighing job offers while planning your MFT education, ask prospective employers directly about these extras. Exploring broader MFT career paths can help you identify which workplace settings are most likely to offer generous tuition benefits. A position that pays slightly less on paper but covers tuition and practicum hours can be worth far more over the life of your degree.

If your employer offers tuition reimbursement and you enroll in an online MFT program, you can effectively earn while you learn and have your employer subsidize the degree. This combination can cut total out of pocket costs by 25 to 40 percent over a two to three year program, making graduate education significantly more accessible without career interruption.

Online Vs. Campus MFT Programs: Cost and Financial Aid Differences

Choosing between an online and a campus-based MFT program affects more than just your daily schedule. It shapes your total cost of attendance, your ability to earn income during school, and the types of financial aid you can access. Both formats can lead to the same COAMFTE-accredited degree and full licensure eligibility, so the decision often comes down to finances and personal circumstances.

Pros

Online programs typically cost less overall because you eliminate relocation, housing, commuting, and campus fee expenses.

Students in online programs can maintain full-time employment, offsetting tuition costs with steady income while completing coursework.

Online MFT students qualify for the same federal Direct Unsubsidized Loans, up to $20,500 per year, as their campus counterparts.

Asynchronous online formats offer flexible scheduling that accommodates students with families or demanding work commitments.

Campus programs provide embedded practicum placements, reducing the burden of finding and arranging your own clinical sites.

On-campus students benefit from stronger peer cohort networks and face-to-face faculty mentorship that can support career development.

Many campus-based programs offer graduate assistantships, tuition waivers, and institution-specific scholarships that are harder to find online.

Cons

Online students may have limited access to campus-based scholarships, assistantships, and work-study positions that reduce out-of-pocket costs.

Self-arranging practicum sites is common in online programs, adding logistical complexity and potential travel expenses.

Online learners may miss organic networking opportunities with classmates and local clinical supervisors that campus settings naturally provide.

Campus-based programs carry a higher total cost of attendance once you factor in housing, transportation, and mandatory campus fees.

Attending classes on campus makes it significantly harder to hold full-time employment, reducing income during the degree.

Geographic constraints limit campus students to programs within commuting distance unless they are willing to relocate.

MFT Degree ROI: Is the Investment Worth It?

Earning potential is the clearest lens for evaluating whether MFT program debt is manageable. Nationally, marriage and family therapists earn a median salary of $63,780, but geography dramatically shifts the equation: licensed MFTs in California, for example, earn between $82,000 and $124,000 annually, according to data published by Notre Dame de Namur University in May 2026. When you compare typical graduate debt of $80,000 to $120,000 against these salary figures, a debt-to-income ratio below 1.5 is achievable in higher-paying markets, and even at the national median, most graduates can expect to repay loans within a standard 10-year window. The table below puts the key numbers side by side so you can gauge ROI at different points on the earnings spectrum.

Metric

25th Percentile

National Median

75th Percentile

California LMFT Range

Annual Salary

$48,600

$63,780

$85,020

$82,000 to $124,000

Typical Graduate Debt at Graduation

$80,000 to $120,000

$80,000 to $120,000

$80,000 to $120,000

$80,000 to $120,000

Debt-to-Income Ratio (using $100K midpoint debt)

2.06

1.57

1.18

0.81 to 1.22

Monthly Loan Payment (10-yr, 7% rate, $100K loan)

$1,161

$1,161

$1,161

$1,161

Loan Payment as Share of Gross Monthly Income

28.7%

21.8%

16.4%

11.2% to 17.0%

Funding Options for Non-Traditional MFT Students

Graduate students pursuing an MFT degree can borrow up to $20,500 per year in federal Direct Unsubsidized Loans, regardless of their age or previous career path. This fixed annual limit provides a predictable baseline for financing, whether you're entering directly from an undergraduate program or transitioning from an unrelated field. Non-traditional students, including career changers, part-time learners, international applicants, and military-connected individuals, have access to a wide range of funding sources that align with their unique circumstances.

Federal Aid and Loan Limits for Career Changers

Your eligibility for federal financial aid is not tied to your employment history or undergraduate major. The Free Application for Federal Student Aid (FAFSA) determines borrowing capacity based on the cost of attendance set by your program, not your career background. If you've been out of school for years, the process is identical: complete the FAFSA, accept the offered loans, and consider Grad PLUS loans to cover any remaining gap. Many career changers also qualify for school-based need-based grants, which do not require a traditional academic pathway.

Part-Time Enrollment: Financial Aid Proration and Employer Benefits

Financial aid adjusts when you enroll less than half-time, but it does not disappear entirely. Direct loans are prorated based on your credit load, and you must maintain at least half-time status to remain eligible. The key advantage for part-time MFT students is that employer tuition reimbursement programs often cover expenses across a longer calendar period. Instead of a single $5,250 annual reimbursement, you may access that benefit for each tax year you remain employed while studying, effectively increasing the total employer contribution over the life of your degree.

International Students: Institutional Scholarships and Assistantships

International students are generally ineligible for U.S. federal aid and most national scholarship competitions. However, many COAMFTE accredited MFT programs actively recruit globally and reserve institutional scholarships that do not require domestic residency. Graduate assistantships, paid positions that involve teaching, research, or administrative work, are another viable funding path. These roles often come with tuition waivers and stipends, making the overall cost comparable to what a domestic student might pay after loans. Reach out to program coordinators early to inquire about designated international student awards.

Veteran and Military-Connected Benefits

The Post-9/11 GI Bill and the Yellow Ribbon Program can substantially reduce or eliminate out-of-pocket costs for eligible military veterans, active-duty service members, and dependents. Many MFT programs participate in the Yellow Ribbon Program, matching tuition expenses above the GI Bill cap. Start by requesting a Certificate of Eligibility through the VA, then coordinate with your school's veterans affairs office to apply these benefits directly to tuition and fees. Military tuition assistance programs may also be available for active-duty students enrolled in online MFT programs.

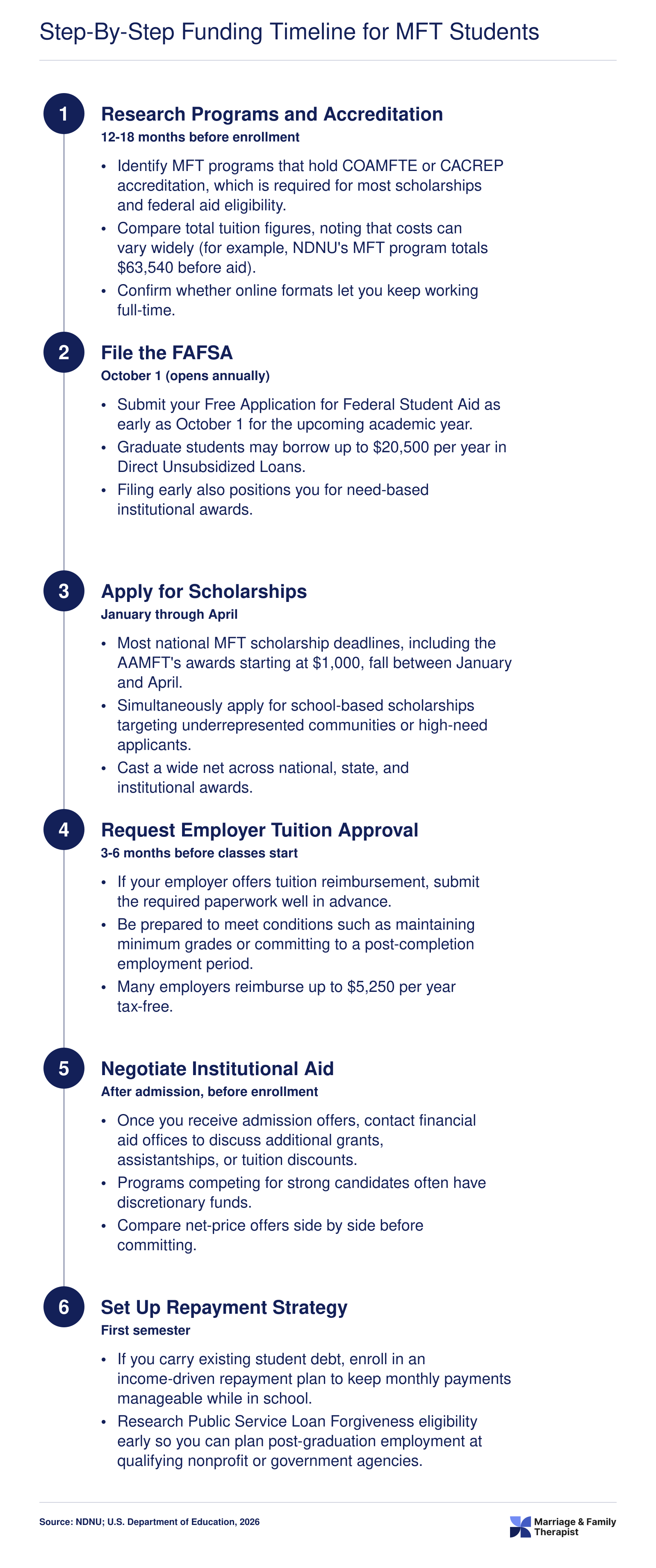

Step-By-Step Funding Timeline for MFT Students

Planning your finances 12 to 18 months before enrollment gives you the best chance of stacking multiple funding sources. Follow this timeline to stay ahead of key deadlines and maximize every dollar available for your MFT degree.

Frequently Asked Questions About Affording an MFT Degree

Below are the questions prospective MFT students ask most often about paying for their degree. Each answer gives you a concise starting point; for deeper detail, refer to the corresponding section earlier in this guide.

How much does it cost to become a marriage and family therapist?

Total tuition for a master's in MFT typically ranges from roughly $30,000 at public universities to more than $100,000 at some private institutions. As one concrete example, Notre Dame de Namur University lists its program at $63,540 before financial aid. Costs vary widely by format, residency status, and institution type. See the 'How Much Does an MFT Degree Actually Cost?' section above for a fuller breakdown of what drives those differences.

What scholarships are available specifically for MFT students?

MFT students can tap three tiers of scholarships. At the national level, the American Association for Marriage and Family Therapy (AAMFT) offers awards starting at $1,000 for graduate students. State counseling associations and diversity focused foundations add another layer. Many COAMFTE accredited programs also provide their own institutional scholarships, including need based awards for students from underrepresented communities. The scholarships section of this guide details how to find and stack these awards.

Can LMFTs qualify for student loan forgiveness?

Yes. Licensed marriage and family therapists who work full time for qualifying nonprofit or government employers may be eligible for Public Service Loan Forgiveness (PSLF) after 120 qualifying monthly payments under an income driven repayment plan. Some state programs offer additional forgiveness for mental health professionals serving underserved populations. Review the 'Loan Forgiveness and Service Obligation Programs' section for eligibility steps.

Does winning a scholarship reduce my other financial aid?

It can. Under federal rules, your total aid cannot exceed your cost of attendance. If a new scholarship pushes you over that limit, your school may reduce other aid, often starting with loans rather than grants. This actually benefits you because it lowers the amount you borrow. Always notify your financial aid office when you receive an outside award so they can adjust your package in the most favorable way possible.

How do scholarship for service programs work for MFT graduates?

These programs cover part or all of your tuition in exchange for a commitment to practice in a high need or underserved area after graduation. The service obligation typically lasts two to four years. If you do not fulfill the commitment, the award usually converts to a loan that must be repaid with interest. The 'Loan Forgiveness and Service Obligation Programs' section explains how to locate these opportunities and what to expect from the commitment.

Is an MFT degree worth the cost?

For most graduates, the return on investment is strong. In California, for instance, licensed MFTs earn a median salary between $82,000 and $124,000 per year. Even at a program price near $63,540, many graduates recoup their investment within a few years of licensure. The 'MFT Degree ROI' section above walks through a detailed comparison of earnings versus typical loan payments so you can run the numbers for your own situation.

Do online MFT programs qualify for the same financial aid as campus programs?

Yes, provided the program holds proper accreditation. Students enrolled in accredited online MFT programs are eligible for the same federal Direct Unsubsidized Loans (up to $20,500 per year), institutional scholarships, and employer tuition reimbursement as their on campus peers. Online formats also let you work full time while studying, which can significantly reduce how much you need to borrow. The 'Online vs. Campus MFT Programs' section compares cost and aid differences in greater detail.

The gap between a program's sticker price and what you actually pay is often substantial. As the net-price case study above illustrates, stacking just two or three funding sources, such as federal Direct Unsubsidized Loans, a school-based scholarship, and employer tuition reimbursement, can cut tens of thousands of dollars from your total bill.

Your first concrete step is simple: file the FAFSA. That single action unlocks up to $20,500 per year in federal loans and positions you for institutional aid. From there, work through the scholarship table in this guide and contact your employer's HR department about tuition benefits. With California LMFTs earning $82,000 to $124,000 annually, a strategically funded MFT degree pays for itself. The investment is sound; your job is to minimize the debt attached to it. If you are still comparing programs by cost, our list of best value MFT programs can help you narrow the field before you apply.